As global awareness and concern for sustainable development goals (SDGs) continue to rise, corporations are increasingly expected to prioritise SDGs by aligning their environmental, social, and governance (ESG) goals. Governmental initiatives and investor preferences are reinforcing this shift towards a more sustainable business model. Governments worldwide, including in India, are actively pursuing legislative changes to address pressing challenges like mitigating the impact of climate change by promoting sustainable business practices. Also, investors are recognising the significance of ESG factors as essential for impactful investments and a better future for all on the planet.

Voluntary CSR and Compulsory BRSR

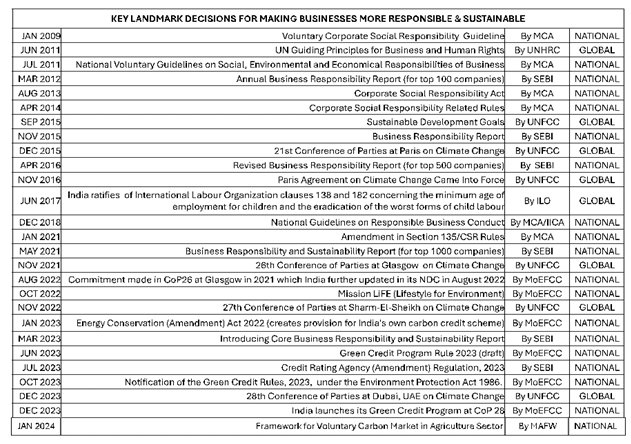

In the Indian context, the announcement of voluntary corporate social responsibility in Dec 2009 by the Ministry of Corporate Affairs (MCA), set the tone for the ESG journey for corporations. The fundamental principle of voluntary CSR as highlighted in the guiding document[1] was that ‘each business entity should formulate a CSR policy to guide its strategic planning and provide a roadmap for its CSR initiatives, which should be an integral part of overall business policy and aligned with its business goals and should be approved by the Board”. This guiding document also highlighted six core elements: (1) care for all stakeholders (2) ethical functioning (3) respect for workers’ rights and welfare (4) respect for human rights (5) respect for the environment and (6) activities for social and inclusive development.

Further, in 2011, MCA introduced the refined version of this document named ‘National Voluntary Guidelines on Social, Environmental and Economical Responsibilities of Business’[2] (NVG), in which the six core elements of voluntary CSR, as mentioned above, were extended by adding three new principles, covering almost all key aspects of business functioning to make businesses more responsible and sustainable. Subsequently, in 2012, the Securities Exchange Board of India (SEBI) amended the listing agreement for companies listed in the stock exchanges in India and mandated the submission of an Annual Business Responsibility Report (ABRR) by the top 100 listed companies.

In the year 2013, based on the principle number 8 of NVG (i.e. Businesses should support inclusive growth and equitable development), India became the first country to pass the Corporate Social Responsibility Act of 2013, which was later amended in January 2021.[3] Under this act, the Board of companies who have either a net worth of rupees 500 crore or more, or turnover of rupees 1000 crore or more, or a net profit of rupees 5 crore or more should ensure that the company spends, in every financial year, at least 2 per cent of the average profit as CSR (profit before tax).

In line with the CSR Act of 2013, a revised format for the Business Responsibility Report (BRR) was also introduced in November 2015 by SEBI. Top 500 companies, based on market capitalisation, (earlier 100) were included under annual voluntary reporting from April 2016. However, as uptake of this voluntary reporting ended up not being up to the satisfactory mark, MCA with the technical support of the Indian Institute of Corporate Affairs (IICA), developed the National Guidelines on Responsible Business Conduct[4] (NGRBC) in 2018 to help companies prepare their annual BRR reports.

Again in May 2021, the BRR format was replaced with BRSR (Business Responsibility and Sustainability Report) by SEBI to make Indian companies’ ESG reporting aligned with global sustainability reporting frameworks, such as the Global Reporting Initiative (GRI) and the United Nations Global Compact (UNGC) to enhance the quality of sustainability reports by listed entities in India. The purview of BRSR was extended to the top 1000 companies, as they were asked to volunteer to report on the adherence to the 9 principles proposed covering almost 800 parameters. In 2022-2023 BRSR reporting was made mandatory.

Global Development Agendas and ESG Goals

Environmental, Social, and Governance (ESG) frameworks, align with several global development agendas and compliance initiatives that play a pivotal role in holding companies more accountable to society and the environment. Significant events such as the introduction of the UN Guiding Principles for Business and Human Rights (UNGPs) in 2011, the Paris Agreement on Climate Change in 2015, which set legally binding goals to limit global temperature rise, and the subsequent Nationally Determined Contributions (NDCs) by all countries, including India, underscore the emphasis on alignment and need for urgent action on pressing causes. Furthermore, India’s ratification of International Labour Organization clauses 138 and 182 concerning the minimum age of employment for children and the eradication of the worst forms of child labour in 2017, alongside commitments made in forums like CoP26 at Glasgow in 2021 and the subsequent update to India’s NDC in August 2022, demonstrate a growing resolve to address global societal challenges.

Notably, the outcomes of the CoP28 UN Climate Change Conference held in Dubai, in November-December 2023, marked by an agreement signalling a transition away from the fossil fuel era, underscore the urgency and importance of the ESG agenda. Such events nudge businesses to embrace more responsible and sustainable practices and emphasise the necessity for businesses to integrate ESG considerations into their core strategies and operations.

Strengthening the Impact Measurement System

Despite measures to strengthen regulations, unregulated ESG rating providers (ERPs) are an area of concern, diluting the essence. SEBI has expressed concern about the activities of unregulated ERPs which may lead to further challenges around investor protection, market efficiency, risk pricing, and greenwashing. To address these concerns, two key changes have been brought recently: First, SEBI introduced the concept of core BRSR reporting in March 2023, which mandates 49 parameters for ESG reporting, down from 800 previously. The new reporting aims to establish linkages between the financial results of a business and its ESG performance. This will make it easier for regulators, investors, and other stakeholders to obtain a fair estimate of the overall stability and growth of the business. Second, is the introduction of SEBI (Credit Rating Agency) (Amendment) Regulations, 2023 on 3rd July 2023[5]. This regulates the ESG rating agencies and mandates that no person/company shall act as an ESG rating provider unless they hold a certificate from SEBI, to ensure the veracity of ESG reporting.

Sustainability Fund for ESG

Full compliance with Environmental, Social, and Governance (ESG) goals necessitates a significant amount of sustainability funds. Though the social commitment (of ESG) will largely come from the Corporate Social Responsibility (CSR) fund, the growing need for resources may also lead to a potential redirection of some CSR funds towards companies’ environmental commitment (of ESG) by investing more in green CSR projects which will also create surpluses like reduced carbon emissions or water savings. For instance, the recently introduced “Framework for Voluntary Carbon Market in Agriculture Sector”[6] by the Ministry of Agriculture and Farmers’ Welfare encourages companies and individuals to take responsibility for their carbon emissions and invest in projects that have a positive impact on the environment and local communities and how by purchasing carbon credits from agriculture projects in India buyers can contribute to sustainable development goals. Framework document also highlights the demand for carbon credits as numerous large corporations have set net-zero targets and many more are expected to do so over this decade.

However, under the current CSR regulations, any surplus resulting from CSR activities cannot contribute to a company’s business profit and must be reinvested in the same project or transferred to the unspent CSR account. Therefore, it is anticipated that the Ministry of Corporate Affairs (MCA) will issue this crucial clarification on whether companies should (or should not) utilize CSR funds to meet some of their environmental commitments, particularly concerning carbon offsetting and achieving water neutrality or positivity. Nevertheless, achieving ESG goals will demand substantial investments beyond CSR funds. Therefore, organizations must explore innovative financing mechanisms and strategic partnerships to bridge the gap between financial requirements and sustainability targets by creating realistic sustainability funds.

Conclusion

In conclusion, the mandatory shift towards CSR and core BRSR in India and strong regulations by organisations like the MCA and SEBI, amendments in India’s Energy Conservation (Amendment) Act, 2022[7], which creates provision for India’s carbon credit scheme, the launch of the Green Credit Initiative at[8]CoP28 in December 2023 and India’s climate change related legally binding NDCs (Nationally Determined Contributions) demonstrate a commitment to addressing societal and environmental challenges with businesses as a lever.

As businesses increasingly integrate sustainability into their core strategies and operations to meet these regulatory requirements and tackle global challenges like climate change, those at the forefront of this transition stand to gain a competitive advantage. By embracing ESG principles, organizations not only contribute to environmental and social well-being but also position themselves as leaders in a rapidly evolving landscape of responsible business practices.

[1] CSR Voluntary Guidelines 24dec2009.pdf

[2] National Voluntary Guidelines 2011 12jul2011.pdf

[3] EBook

[4] National Guildeline 15032019.pdf

[5] Securities and exchange board of india credit rating agencies amendment regulations 2023

[6] Framework for Voluntary Carbon Market 1-Feb-2024 Revised

[7] The Energy Conservation (Amendment) Act, 2022.pdf

[8] Draft GCP Notification Inviting Comments 27062023.pdf

Author

Pranav Kumar Choudhary | COO

AI and critical thinking in education: The Answer Came Too Easily

AI in Promotions: Should AI Decide Who Gets Promoted?